Hysteria on Danish stock market - or how to tickle the small shareholders up their backs! UPDATED TWICE

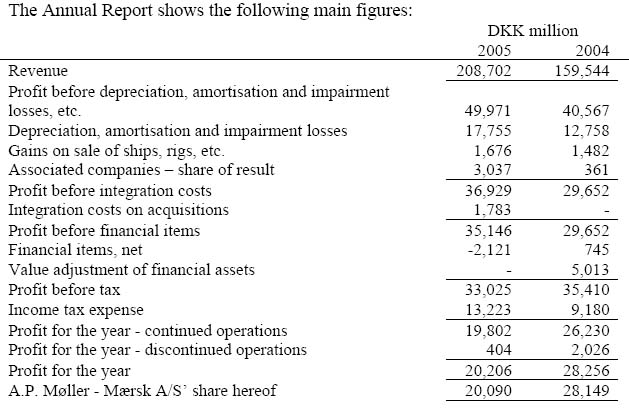

APM-Maersk Report and accounts for 2005

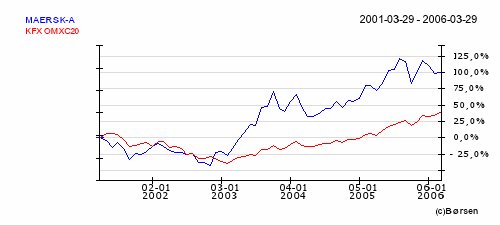

A-share March 29 06

(Maersk A share (blue) and general Copenhagen index. 5 year development)

Mass hysteria broke out on the Danish stock exchange today, proving that mass psychosis is part of the behaviour pattern of investors and stock exchanges, at least as much or even more than hard economic facts.

The big company A.P. Moller Maersk, which stands for 12-13 per cent of the Danish production (GNP), published its yearly report and accounts for 2005 today.

Investors reacted solely on the bottom line, which was not quite so much in surplus as in 2004, even though the very profits of this company corresponds to more than half the gross national product of a mid-size African country. The two shares, Maersk A and B that comprise about 1/3 of total market trading of the Danish stock exchange's C20 index of the 20 most traded shares, fell by 15 per cent in mid afternoon. That corresponded to 40 bn. kroners (6-7 bn. $) wiped off the market value of the firm.

Most of the reaction is pure mass hysteria. A closer look at numbers (at link or above) shows that most of the decline is due to acquisition of the Anglo-Dutch P&O Netlloyd container line in 2005 and amortisaton of investment in oil fields in the British sector of the North Sea. This has led to increased depreciation and financial costs. These investments will pay off after some time and increase profits. The lower value of British sector oil fields is a pure estimate. No outsiders can verify this. It gives the company room for bringing down 2005 profits. The heavy depreciation costs - "luckily" - keeps profits fairly moderate, thus producing "political correctness" accounts. Maersk traditionally makes "conservative" accounts, systematically moderating income projections. In this case the company has a clear interest in not provoking more public clamour over the 2003 deal with the state (explained below).

Financial analysts have noted that profit before tax was bigger in 2004 than in 2005, but in 2004 there was a one-time item of 5 bn. D.kr, i.e. value adjustment of financial assets.

Furthermore, in spite of increased depreciation costs, Maersk pays increased taxes. This is surprising at a time when Danish corporation taxes have been reduced to only 28 per cent. The company clearly sees an interest in getting tax payments up. Postponed tax from previous years will be paid in 2005. Why is that? Why is the company p(l)aying Santa Claus to the Danish state?

In 2003 Maersk negotiated an agreement with the Danish state that is astounding both in legal procedure and results. The state makes a tax agreement with a single private interest. And it was extremely beneficial for this private interest:

The company was given sole rights to pump oil in its part of the North Sea until 2042, with no option for the state to terminate the contract. Oil taxes were based on the low oil prices prevailing until 2003. After that oil prices more than doubled making it possible for the company to shovel money in. Furthermore, the treaty says that if the Danish state increases taxation on oil, the company has a right to be compensated.

There has been some criticism in the media lately of this astoundingly beneficial deal - beneficial for Maersk and its shareholders. The left party the Unity List is trying to bring up the matter in the Danish parliament.

So, what has happened is probably something which is not uncommon in the corporate world: "This was the report we chose to present this year." Public discontent must be cooled off a bit. If we can make the bottom line look somewhat less rosy than it actually is, it is good for us in the long run.

Who is going to pay for this exercise in corporate communication? The common shareholder, who has invested his or her pension money in Maersk shares, and who sells in the course of the panic selling this afternoon. Who is going to win?:

The big investors who sit on the side line and bemusedly watch the show and buy when the stock has presumably hit bottom. Because it'll rise again eventually. A closer look at the numbers above clearly demonstrate it! According to Danish business paper Borsen, when American investors woke up at opening hour on Wall Street, which was mid afternoon in Copenhagen, they sent the stock further down in new panic selling. At the closure of the Danish stock exchange it had regained quite a lot of ground. Sorry for the little investor: You lost again!

Latest: The stock exchange has informed the public that the chairman of the board of Maersk Michael Pram Rasmussen has bought 20 A stocks when the stock was down thursday afternoon. He has to inform the stock exchange of this according to insider trading rules. This is interesting: He may have done so to regain faith in the stock. He may also be acting out of knowledge of the kind referred to above: The stock is undervalued at the exchange because of cautious accounting practices. It's hard to say whether the books are "cooked" or not. They're probably not so in an illegal sense. Danish accounting legislation, however, leaves quite a lot to estimate. There may be much arbitrary value fixation. At Maersk they call it cautious principles of accounting.

A-share March 29 06

(Maersk A share (blue) and general Copenhagen index. 5 year development)

Mass hysteria broke out on the Danish stock exchange today, proving that mass psychosis is part of the behaviour pattern of investors and stock exchanges, at least as much or even more than hard economic facts.

The big company A.P. Moller Maersk, which stands for 12-13 per cent of the Danish production (GNP), published its yearly report and accounts for 2005 today.

Investors reacted solely on the bottom line, which was not quite so much in surplus as in 2004, even though the very profits of this company corresponds to more than half the gross national product of a mid-size African country. The two shares, Maersk A and B that comprise about 1/3 of total market trading of the Danish stock exchange's C20 index of the 20 most traded shares, fell by 15 per cent in mid afternoon. That corresponded to 40 bn. kroners (6-7 bn. $) wiped off the market value of the firm.

Most of the reaction is pure mass hysteria. A closer look at numbers (at link or above) shows that most of the decline is due to acquisition of the Anglo-Dutch P&O Netlloyd container line in 2005 and amortisaton of investment in oil fields in the British sector of the North Sea. This has led to increased depreciation and financial costs. These investments will pay off after some time and increase profits. The lower value of British sector oil fields is a pure estimate. No outsiders can verify this. It gives the company room for bringing down 2005 profits. The heavy depreciation costs - "luckily" - keeps profits fairly moderate, thus producing "political correctness" accounts. Maersk traditionally makes "conservative" accounts, systematically moderating income projections. In this case the company has a clear interest in not provoking more public clamour over the 2003 deal with the state (explained below).

Financial analysts have noted that profit before tax was bigger in 2004 than in 2005, but in 2004 there was a one-time item of 5 bn. D.kr, i.e. value adjustment of financial assets.

Furthermore, in spite of increased depreciation costs, Maersk pays increased taxes. This is surprising at a time when Danish corporation taxes have been reduced to only 28 per cent. The company clearly sees an interest in getting tax payments up. Postponed tax from previous years will be paid in 2005. Why is that? Why is the company p(l)aying Santa Claus to the Danish state?

In 2003 Maersk negotiated an agreement with the Danish state that is astounding both in legal procedure and results. The state makes a tax agreement with a single private interest. And it was extremely beneficial for this private interest:

The company was given sole rights to pump oil in its part of the North Sea until 2042, with no option for the state to terminate the contract. Oil taxes were based on the low oil prices prevailing until 2003. After that oil prices more than doubled making it possible for the company to shovel money in. Furthermore, the treaty says that if the Danish state increases taxation on oil, the company has a right to be compensated.

There has been some criticism in the media lately of this astoundingly beneficial deal - beneficial for Maersk and its shareholders. The left party the Unity List is trying to bring up the matter in the Danish parliament.

So, what has happened is probably something which is not uncommon in the corporate world: "This was the report we chose to present this year." Public discontent must be cooled off a bit. If we can make the bottom line look somewhat less rosy than it actually is, it is good for us in the long run.

Who is going to pay for this exercise in corporate communication? The common shareholder, who has invested his or her pension money in Maersk shares, and who sells in the course of the panic selling this afternoon. Who is going to win?:

The big investors who sit on the side line and bemusedly watch the show and buy when the stock has presumably hit bottom. Because it'll rise again eventually. A closer look at the numbers above clearly demonstrate it! According to Danish business paper Borsen, when American investors woke up at opening hour on Wall Street, which was mid afternoon in Copenhagen, they sent the stock further down in new panic selling. At the closure of the Danish stock exchange it had regained quite a lot of ground. Sorry for the little investor: You lost again!

Latest: The stock exchange has informed the public that the chairman of the board of Maersk Michael Pram Rasmussen has bought 20 A stocks when the stock was down thursday afternoon. He has to inform the stock exchange of this according to insider trading rules. This is interesting: He may have done so to regain faith in the stock. He may also be acting out of knowledge of the kind referred to above: The stock is undervalued at the exchange because of cautious accounting practices. It's hard to say whether the books are "cooked" or not. They're probably not so in an illegal sense. Danish accounting legislation, however, leaves quite a lot to estimate. There may be much arbitrary value fixation. At Maersk they call it cautious principles of accounting.

posted by Cosmic Duck at 6:12 AM

![]()

![]()

0 Comments:

Post a Comment

<< Home